Navigating Innovation amidst economic uncertainty of 2024 - Recession recovery looking at 2025

“While many governments still struggle with the massive amounts of public debt accumulated during COVID, the business sector has continued to increase its levels of innovation. However, this trend may hide growing disparities, as some sectors have attracted significant funding (typically artificial intelligence) while gaps have started to appear in the financing chain, especially venture capital for small and new businesses. Against the background of growing trade tensions and lower levels of international cooperation, such trends could hamper the ability of innovative firms to fully contribute to the resumption of sustainable growth.”

The above remark is by the Global Innovation Index Co-Editor Bruno Lanvin, it is something that we in RVmagnetics felt on the ground level, and as it resonates with our clients, partners, strategic investors and the buzz we’ve been hearing and attending to, over 2023 and now through 2024 as well. We felt it relevant to share the overview with our audience from a prism of specifically an R&D entity, a deeptech startup based in the EU.

Now, with more than two thirds of 2024 gone – what should any company, industry or private entity be on the lookout for in regards to Research, Development and the reality around? Let us share our experience.

A Quick Overview of RVmagnetics:

We are a deeptech startup , currently the majority of our activities is developing and manufacturing measurement and sensing solutions for niche demand – for a pool of clients and partners that have a physical data acquisition challenge, which hasn’t been able to be solved by other sensing, measurement, detection and tracking technologies.

Our Solution

It is based on our proprietary MicroWire sensors, thin, elastic like human hair, with no need for power wiring, these sensors help our clients and partners to get physical data from otherwise inaccessible spaces. This data can be a measurement of pressure, temperature, mag. field, vibrations, torsion, el. current, or even simply Identification of MicroWire.

Our Market

Due to the volume and value of the measurement challenges we can solve, we have generated a rather high interest from variety of industries (i.e. aviation, automotive, construction, food & beverage, water tech, medical tech, industrial automotive, etc.), and industry players of medium to large sizes especially (including Tier 1 companies in Automotive and Aviation, and Fortune 500’s representing diverse industries). The interest is not just theoretical, we have been developing projects of high Technology Readiness Levels (TRL), and stepping into the Mass Manufacturing spaces. The clientele is from western EU, Japan, USA and rapidly developing economies such as Brazil, India and China. Some of our main applications are for Composite Materials, Electric Motors, Batteries (EVs, rechargeable,) and Industrial Automation.

Our Challenges

They are not few – being the only company manufacturing these MicroWire sensors and offering the application development comes with its pros and cons. The cons are connected with longer customer flow than within a usual, already rather lengthy R&D process. Not only we need to Proof the Conceptual relevance, we cannot have a catalogue of sensors fit-for-all, our approach must be exclusive and unique for our clients. Luckily our partners and clients realize the value and RoI from the implementation of the MicroWire tech, at the same time however, we are still a scale-up, that works with numbers of corporations – and corporations, in order to stay afloat in a short run, may hold R&D spendings. A good example of this, was the 2022 Microchip shortages with its damaging affects for the automotive, and with a sharp shadow in 2023.

Specifically in 2023, the market dynamics in the EU have had their effects on our partners and clients, thus naturally on us as well. Since the economic shutdowns of 2020, we have learned how to navigate our strategies in these spaces of R&D spending, identifying where are our solutions the most useful and the quickest to adopt. At the start of the year, we looked at some relevant sources and tried to conclude what’s coming in 2024. We are happy to share this with our audiences, including peer startups, potential partners and investors.

R&D Landscape in 2024: The Role of Startups, Corporations, and Academa Amid Global Shifts

In 2024, the global R&D ecosystem is transforming “gracefully”. It is driven by political, economic, and technological shifts mostly. With elections in key regions like the US Southern Asia, EU connected with the evolving government policies and corporate strategies, the innovation dynamics alone are going through significant reconfigurations. Companies, especially those in highly competitive industries, must adapt to new realities in R&D funding, partnerships, and innovation strategies to maintain their market edge and drive technological progress.

Sure, you may go back 5 years, read the above sentence and it would be just as relevant, but 5 years ago, the stars did not align quite like they have now – talking about inflation, war, post-virus realities, numbers of elections in one year, shift in government and large firm decision making in R&D.

This blog explores the above, the current state of R&D in 2024, highlighting the crucial interplay between startups, corporations, and academia. We will deepdive into how political decisions, economic trends, and resulting advancements in technology shape R&D investments, the role of open innovation, and the still-growing importance of science-backed startups as engines of innovation.

Global R&D Investment Trends in 2024: A Focus on Growth and Sector Shifts

The way we in RVmagnetics understand and view it, R&D is the lifeblood of innovation and economic competitiveness. As of 2024, global R&D spending continues to grow, reaching new heights as both public and private sectors invest in technological advancements. We are one of the inspired investors of our time and capacity in “communal” growth of global R&D as we represent innovative applications with our top-tier partners and we do feel the effect of this modern world on us.

On a more global level, the US and China dominate this landscape (still), together accounting for nearly 60 % of the global total, while other countries such as Korea and Israel stand out for their high R&D intensity.

Global R&D Spending Overview

Global R&D investment has grown substantially over the past three decades, tripling from $672 billion in 1992 to over $2.2 trillion by 2021. The U.S. leads with 32 % of global R&D funding, followed by China at 27 %, which continues to rapidly increase its R&D efforts.

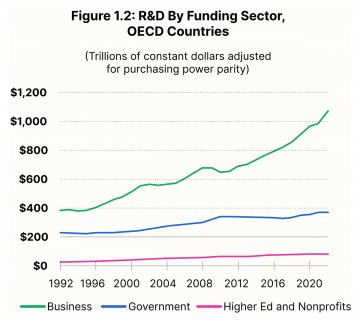

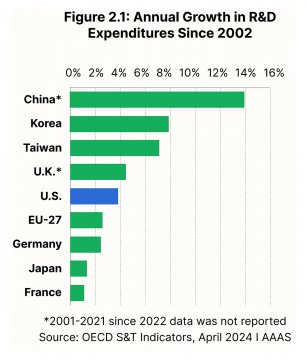

However, China being a non-OECD entity, bends some of the comparative metrics in global R&D as OECD countries have experienced a step up in their R&D intensity (at around 2.7 % of GDP). Based on the “R&D World” and the “NSF” notes – R&D by Sector in OECD Countries – businesses are the dominant force in R&D investment, contributing over $1.07 trillion in 2022 (63% of the total).Government funding comes at 22%, and the remaining 15% comes from unis and nonprofits. Going back all the way to 1992, business R&D has more than doubled, while government R&D funding has increased only by 64%.Countries like Taiwan, Korea, and China are leading the charge in terms of annual R&D growth, largely driven by government policies promoting innovation as a key pillar of economic development. Korea, for example, is recognized as one of the most R&D-intensive nations, with significant government and business contributions to research initiatives.

The US is still the largest spender but now facing a slower growth compared to these Asian competitors. In fact, while the US ranks 4th in terms of overall R&D intensity (R&D as a share of GDP), other countries like Israel and Korea devote a larger portion of their economic output to innovation.

Future Projections and Industry Contributions

Looking ahead, industrial R&D is expected to dominate global efforts, especially in sectors such as artificial intelligence (AI), biotechnology, and renewable energy. Korea, Taiwan, and other countries adopted tax incentives and fostering public-private partnerships to encourage more R&D spending. Meanwhile, the US is focusing on areas like clean energy and AI, heavily influenced by their 2022 Inflation Reduction Act.

In 2024, the global R&D landscape is shaped by both competition and collaboration. While the U.S. remains a dominant player, its relative share is being challenged by fast-growing economies like China, Korea, and Taiwan. The future of R&D will depend heavily on public-private partnerships, cross-border collaborations, and the continued prioritisation of innovation as a key economic driver.

Within a year with so many elections and political changes ahead, let’s explore the above topic in 4 pillars: R&D Investments in 2024: Economic and Political Drivers; Science-Backed Startups: Catalysts for Corporate R&D in 2024; Emergence of Open Innovation: Collaboration for Competitive Advantage; Future of R&D in 2025 and Beyond: A Collaborative Innovation Ecosystem.

1. R&D Investments in 2024: Economic and Political Drivers

2024 is a year marked by heightened geopolitical uncertainty, impacting R&D investments globally. In the United States, the ongoing presidential election cycle has introduced volatility to government-backed R&D funding, as candidates propose diverging policies on science, technology, and innovation. There is anticipation of increased funding in specific areas such as clean energy, digital infrastructure, and healthcare, influenced by policy platforms focused on addressing climate change and economic recovery post-pandemic. However, uncertainty about the future direction of U.S. R&D funding may lead companies to hedge their bets and focus more on private-sector partnerships and external innovation to minimise risks.

Government R&D Spending: Navigating Policy Shifts

In 2023, U.S. federal R&D investment reached approximately $181 billion, with a significant portion allocated to defence, healthcare, and energy sectors. Looking ahead, there is speculation that 2024 government R&D budgets will either increase or shift priorities depending on election outcomes this November. Environmental, social, and governance (ESG) regulations are expected to become more stringent, particularly in the European Union, influencing corporate investment strategies in green technologies. In fact total government budget allocations for R&D (GBARD) in the EU reached 0.73 % of GDP in 2023, reflecting a 5.3 % increase from the previous year. This amounted to €123.7 billion, which highlights a continuing upward trend in R&D funding according to the European Commission, but upcoming elections and the European Green Deal’s implementation will likely accelerate the transition toward sustainable innovation in 2024 and beyond.

In China, the government’s long-term focus on becoming a global technology leader has led to massive R&D investments, particularly in artificial intelligence (AI), semiconductors, and biotechnology. The Made in China 2025 plan aims to boost domestic innovation while reducing dependence on foreign technologies, pushing both state-owned and private enterprises to invest heavily in R&D.

Defence and EU

In 2024, the global landscape of R&D is being driven by a delicate balance between innovation in defence technologies and a surge in clean energy initiatives. The rapid development of defence technologies is being shaped by rising geopolitical tensions, prompting nations—particularly in the EU—to increase their investments in autonomous systems, cybersecurity, and aerospace. This shift is part of a broader strategy to ensure military readiness and technological superiority. Countries are now increasingly channelling resources into R&D to develop more resilient defence infrastructures. EU policies, in response, are actively evolving to accommodate these defence needs, focusing on projects that bolster security and preparedness for potential conflicts.

Simultaneously, there is a growing focus on sustainability, particularly through hydrogen technology. The EU’s commitment to advancing hydrogen-based projects reflects a larger trend toward cleaner energy. With €1.4 billion earmarked for hydrogen innovation, the continent is accelerating its work on hydrogen mobility and transport applications, aiming to lead the world in decarbonization efforts. This investment is designed to establish Europe as a major player in the hydrogen economy, with an eye on 2025 goals.

For industries and businesses navigating this evolving landscape, the challenge lies in capitalising on these emerging opportunities. Whether it's innovating within the defence sector or pushing the boundaries of sustainable technologies like hydrogen, companies must remain agile and forward-thinking. By focusing on both areas, organisations can drive growth while contributing to a more secure and sustainable future.

Just as prototyping is critical for ensuring the success of a new product, adapting to these R&D trends requires a similar iterative approach. Testing, refining, and continuously evolving ideas in defence and hydrogen technologies will be key to staying competitive.

Inflation and Firms’ Feedback:

In 2024, inflation is a major factor shaping R&D investments for firms and large corporations. High inflation has led to increased costs for materials, labour, and operations, forcing companies to reassess their R&D strategies. Many firms are focusing on optimising costs and delaying or cancelling projects that don't promise immediate returns. For example, a survey found that pharmaceutical companies are shifting their focus away from small molecule medicines and deprioritizing early-stage pipeline projects due to the impact of the Inflation Reduction Act and rising costs.

Inflation also pushes companies to be more cautious with long-term R&D investments, as uncertainties around future costs and revenues grow. This has prompted some firms to divert R&D funding toward safer, short-term innovations rather than groundbreaking, high-risk projects.

Looking ahead to 2025, inflation is expected to moderate, but the lingering effects of rising costs will continue to influence R&D decision-making. Many firms will likely focus on digital transformation and automation to reduce operational expenses while maintaining their innovation capacity.

The Role of Private-Sector R&D: Industry-Led Innovation

While government funding for R&D is crucial, the private sector remains the dominant force in driving innovation. Companies in sectors such as high-tech, pharmaceuticals, automotive, and aerospace continue to account for the majority of global R&D spending. Within 2024, global private-sector R&D investments are expected to surpass $1.5 trillion, with tech giants such as Amazon, Alphabet, Huawei, and Apple leading the charge.

The ongoing semiconductor shortage, competition within the EV market, and advancements in battery technology have intensified corporate R&D efforts. In the U.S., companies like Ford and General Motors are revitalising their previously closed plants, investing billions in EV manufacturing and related R&D projects. Similarly, companies are increasingly investing in sustainable technologies to align with consumer demands and regulatory pressures, spurred by ESG criteria that are reshaping corporate governance worldwide.

2. Science-Backed Startups: Catalysts for Corporate R&D in 2024

Startups, especially those originating from academic research, are playing an increasingly important role in shaping corporate R&D strategies. In 2024, we see a marked shift in how corporations approach innovation, with many opting to partner with startups for specialised R&D tasks. This trend is driven by the agility and flexibility that startups bring, allowing established companies to experiment with cutting-edge technologies without committing vast internal resources.

Academic Research and Commercialization: A Synergistic Relationship

Universities and research institutions have long been the incubators of breakthrough technologies. In 2024, the growing collaboration between academia and startups is becoming essential for the commercialization of complex technologies, particularly in fields such as biotechnology, AI, and renewable energy. Startups serve as the bridge between theoretical research and practical application, offering corporations an efficient route to market-ready innovations.

For instance, deep-tech startups—often spun out of university research labs—are increasingly being courted by large corporations. These startups provide access to revolutionary ideas in fields like quantum computing, genomics, and advanced materials. The reliance on academic startups to drive corporate innovation is particularly evident in sectors with long development cycles, such as pharmaceuticals, where early-stage research is essential for long-term breakthroughs.

Startups and the New R&D Outsourcing Model

Corporations, facing competitive pressures and limited internal R&D capacities, are increasingly outsourcing R&D to science-backed startups. This model allows firms to reduce risks while gaining access to cutting-edge research and development. In 2024, this outsourcing trend is accelerating, particularly in industries like aerospace and defence, where innovation cycles are costly and complex. Moreover, a Bain & Company report highlights that 60 % of companies plan to increase their outsourcing of engineering and R&D activities over this and next 2 years. This shift is part of a broader strategy to address talent shortages, enhance innovation speed, and reduce costs, allowing corporations to focus internal resources on more complex tasks. Collaborating with startups also offers a solution to labour shortages in scientific fields, as large corporations tap into the entrepreneurial talent emerging from universities and research institutions.

Additionally, the rise of government incentives for startup formation, such as R&D tax credits and grants for innovation, is making it easier for companies to partner with startups. These partnerships offer corporations access to breakthrough technologies, while startups gain access to industry expertise, resources, and potential funding from venture capital firms and corporate investors.

3. The Emergence of Open Innovation in 2024: Collaboration for Competitive Advantage

As the R&D landscape evolves, companies are increasingly embracing the concept of open innovation—a collaborative approach where organisations partner with external entities, including startups, academic institutions, and even competitors, to drive technological advancement. This shift is particularly important in 2024, as economic uncertainty and rapid technological change push companies to find more flexible, cost-effective ways to innovate.

The Role of Open Innovation in Driving Corporate R&D

Open innovation allows companies to access external sources of innovation while reducing the cost and risk of developing new technologies internally. For example, large pharmaceutical companies are increasingly relying on open innovation to tap into new drug discovery and development efforts. Rather than building in-house R&D departments from scratch, these firms partner with academic institutions, startups, and even rival companies to collaborate on early-stage research.

In 2024, sectors like high-tech, automotive, and renewable energy are also increasingly turning to open innovation to tackle complex technical challenges. Companies are participating in innovation ecosystems, such as research consortiums and public-private partnerships, to stay ahead of the curve. By pooling resources and knowledge, firms can accelerate the development of new technologies and ensure they remain competitive in fast-evolving markets.

Open Innovation in Practice: Partnering with Startups and Academia

One of the most significant drivers of open innovation in 2024 is the increasing collaboration between corporations, startups, and academia. This model allows firms to leverage academic expertise while benefiting from the entrepreneurial agility of startups. For example, in the automotive sector, companies like Tesla and BMW are collaborating with battery technology startups to develop more efficient, longer-lasting EV batteries. Similarly, tech giants such as Google and Microsoft are engaging with AI startups and research institutions to push the boundaries of machine learning and quantum computing.

Open innovation also fosters the development of industry standards and best practices. By collaborating with external stakeholders, companies can influence the direction of emerging technologies, ensuring that their products align with future market demands and regulatory requirements.

4. The Future of R&D in 2025 and Beyond: A Collaborative Innovation Ecosystem

Looking ahead to 2025, the global R&D landscape is expected to become even more collaborative, with deeper integration between corporations, startups, and academia. Government policies will continue to play a critical role in shaping the direction of innovation, particularly as countries compete for technological leadership in AI, clean energy, and biotech.

Key Trends Shaping R&D in 2025

- AI and Automation: By 2025, advancements in AI and automation will reshape how companies approach R&D. AI-driven tools will become more integral to the research process, helping firms analyse vast amounts of data, identify trends, and accelerate product development.

- Sustainability: The focus on sustainability and green technologies will intensify, driven by global ESG mandates and consumer demand for environmentally friendly products. Corporate R&D strategies will increasingly prioritise innovations in renewable energy, carbon capture, and sustainable manufacturing practices.

- Public-Private Partnerships: Government-backed R&D initiatives, particularly in areas like healthcare and energy (largely now the defence and space), will increasingly involve private-sector collaborations. Countries will continue to invest in large-scale research projects, with corporations and startups contributing expertise and commercial viability.

Conclusion

In conclusion, the R&D ecosystem in 2024 is marked by dynamic collaboration between corporations, startups, and academia, fueled by economic, political, and technological shifts, and, let’s be honest, roller coasters. As open innovation and startup partnerships become more prevalent, companies will need to adapt their strategies to stay competitive in an increasingly complex and interconnected world, the inflation may be softening, which means it’s time to deal with its consequences even more consistently. The future of R&D will be shaped by the ability of the sectors /corporations, startups, academia/ to work together, turning groundbreaking research into commercial, innovative upshot.